Budget Planner Printable

One-Minute Summary

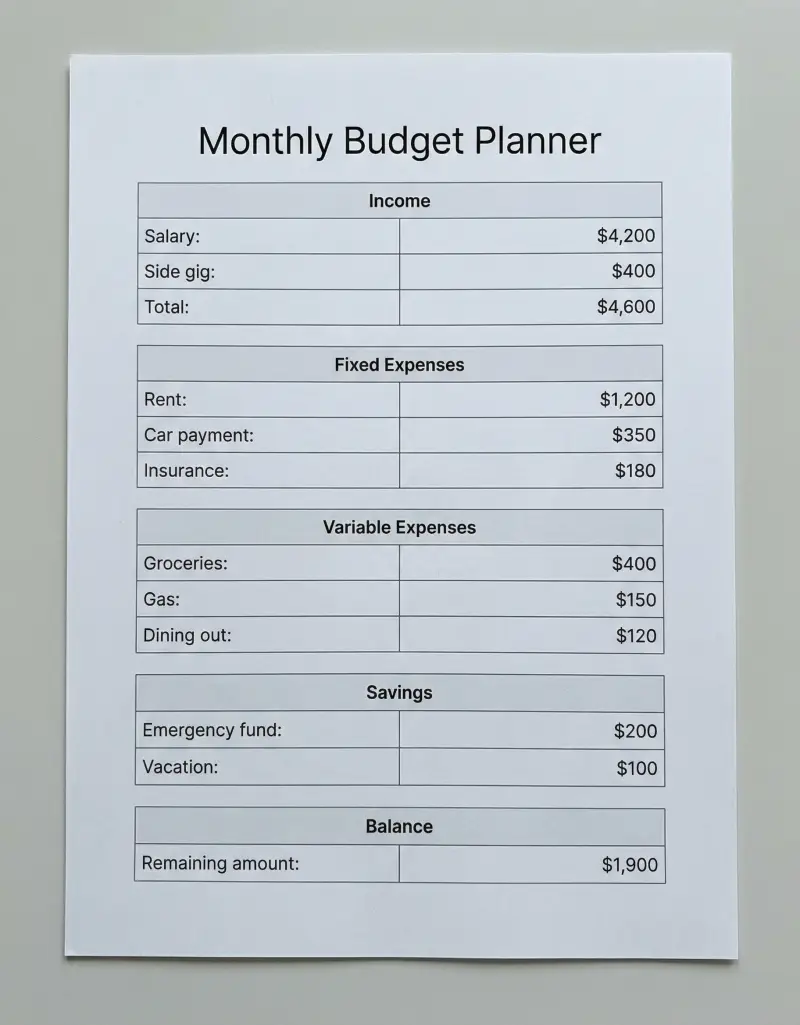

This printable budget planner helps you organize monthly income, fixed expenses (rent, insurance, utilities), variable expenses (groceries, dining, entertainment), savings, and balance. Plan at the start of each month, track as you spend. Print on U.S. Letter paper, keep it visible. This is an organizational tool — it helps you see where your money goes. It is not financial advice.

Preview & Download

Print Settings

- Paper: U.S. Letter (8.5" × 11")

- Orientation: portrait

- Scale: 100%

- Margins: Default (0.5")

- 💡 Print one per month. Keep current month visible. File past months for reference.

What’s on this budget planner

This planner organizes your money into income, fixed expenses, variable expenses, savings, and balance. Fill it in at the start of each month. Track as you go. This is an organizational tool to help you see where your money goes — it is not financial advice.

How to use this planner — 3 real scenarios

Scenario 1: Young professional creating a first budget

You list rent, car insurance, student loan, then estimate groceries, dining, misc. You see the gap between income and expenses. You allocate savings, fun money, and adjust as you learn. The planner gives you a picture you didn’t have before.

Scenario 2: Family tracking two incomes

You and your partner combine incomes, list fixed expenses, allocate variable spending. You review together once a month. The planner keeps you aligned on where money goes instead of wondering where it went.

Scenario 3: Freelancer with irregular income

You use a 3-month average or lowest recent month. You budget fixed first, then variable. Extra income goes to savings or debt. The planner helps you plan for lean months.

Example fill-out

Income: $4,500. Fixed: $1,880. Variable: $870. Savings: $500. Balance: $1,250 — reallocate or adjust.

Common mistakes (and how to fix them)

- Forgetting irregular expenses. Divide annual costs by 12. Add a monthly line.

- Using gross instead of take-home pay. Budget with what lands in your account.

- Being too optimistic about variable spending. Start realistic, adjust down over time.

- Skipping the balance check. Every dollar assigned. If negative, cut somewhere.

- Planning once and never revisiting. Review after 2-3 months. Track actual vs. planned.

Customization tips

Add subcategories under variable expenses. Zero-based approach: income minus allocations = $0. Pay yourself first: savings before variable spending. Review cadence: same day each month.

Printing Tips

- Print on U.S. Letter (8.5" × 11") in portrait orientation

- Scale: 100% (do not use "Fit to Page")

- Margins: Default (0.5")

- 💡 Print one per month. Keep current month visible. File past months for reference.

Next step in your meal prep workflow:

Related Templates You Might Need

Most people use 2–3 of these together:

- •

- •

Helpful Guides

- •

Frequently Asked Questions

What if my income varies every month?

Use your lowest recent month or a 3-month average as your baseline. Budget fixed expenses first. Any month you earn more, allocate the surplus to savings or goals. Build a buffer so lean months don't derail you.

Should I include savings as an expense?

Yes. Treat savings as a fixed line item — pay yourself first. Transfer it on payday before you spend. Even $50/month counts. The planner helps you see it as non-negotiable.

What counts as a fixed vs. variable expense?

Fixed: rent, insurance, subscriptions, loan payments — same amount each month. Variable: groceries, gas, dining, entertainment — changes month to month. Some expenses (utilities) fall in between; put them where they fit.

How detailed should my categories be?

Start with 5-7 total. Add subcategories only if they help. Too much detail causes friction; too little hides overspending. Find the balance that keeps you engaged.

What if I'm consistently over budget?

First, check if your estimates were realistic. Track actual spending for 2 weeks. Adjust your plan to match reality, then gradually trim. Small cuts compound. This is organizational tracking — for debt or savings strategy, research options that fit your situation.

Can I use this with a partner?

Yes. Combine incomes and expenses. Review together monthly. Assign who tracks what. One person can handle the planner; both should agree on the plan. Transparency prevents money conflicts.